You just land at the airport, pull out your credit card to buy a bottle of water, and the shop owner waves you off: “We only accept WeChat or Alipay.”

You open the app you just downloaded, but get a “Identity verification failed” message when trying to bind your card. After finally getting it linked, you’re hit with a 3% “cross-border service fee” when paying…

It’s not your fault—you just need a real payment guide based on the 2026 latest policies.

In 2026, China’s payment policies for foreign tourists have been greatly relaxed. You no longer need a Chinese phone number or bank account—you can directly bind your foreign credit/debit card (Visa, Mastercard, JCB, etc.) to major payment apps. But which of the two platforms is better? How much do they really cost? Do you still need to bring cash?

Today, based on real user feedback from 2025-2026 and the latest official policies, I’ll pit Alipay, WeChat Pay, and cash against each other, and tailor four ultimate payment plans just for you. I’ve tested all these methods myself during my daily life in China, so every tip is tried and true.

Chapter 1: First, Understand the Basics: China’s 2026 Payment Ecosystem

China is highly cashless in 2026. Subways, supermarkets, restaurants, DiDi, and scenic spots all rely almost entirely on QR code payments. But the good news is:

- Greatly optimized policies for foreigners: No need for a Chinese phone number or bank account. You can directly bind foreign credit/debit cards (mainly Visa, Mastercard, JCB, Discover, Diners Club; Amex support is limited) to mobile payment apps.

- Cash is still legal: But acceptance is low (about 30-50% of scenarios), so it’s only for emergencies.

The conclusion is clear: Your main payment method must be mobile payment. And the two major mobile payment players—Alipay and WeChat Pay—have a new showdown in 2026.

Chapter 2: Alipay vs WeChat Pay: 6 Rounds of Head-to-Head in 2026

Round 1: Registration & Real-Name Verification (Who’s More Foreigner-Friendly?)

- ✅ Success rate over 90%, specifically optimized for tourists.

- ✅ Supports an international version interface, with a smooth passport + facial recognition process.

- ✅ Can be bound in advance overseas using WiFi (takes 10-15 minutes).

- ⚠️ Pro Tip: For facial recognition, find a dark background with natural light to avoid AI rejection. I had to try twice because I was in direct sunlight the first time—indoor light works best!

- ⚠️ Success rate 70-80%, a bit “picky”.

- ✅ In 2026, the “need a Chinese friend’s guarantee” activation threshold has been removed, but card binding stability is still not as good as Alipay.

- ❌ Common issues: Not receiving SMS verification codes, review waiting time over 1 day, some card types directly rejected. My friend from Poland tried 3 times before getting his Revolut card linked.

Round 1 Summary: Alipay wins. For most tourists, Alipay’s registration process is smoother and has a higher one-time success rate. I recommend binding Alipay first as your main payment method, and WeChat Pay as a backup.

Round 2: Real Card Binding Success Rate Test (Based on 2025-2026 User Feedback)

Combined with over 200 real cases from Reddit and traveler forums—these are not just official data, but real experiences from people like you:

| Card Type | Alipay Success Rate | WeChat Pay Success Rate | Notes (Real User Tips) |

|---|---|---|---|

| Mainstream Bank Visa/Mastercard Credit Cards | 90%+ | 75-80% | High one-time success rate for common banks like Chase, HSBC, and Barclays. My Chase Sapphire Preferred linked to Alipay on the first try. |

| Neobanks/Virtual Cards (e.g., Wise, Revolut, N26) | 85% | 60-70% | WeChat Pay has stricter risk control for virtual cards. A friend’s Revolut card failed on WeChat but worked perfectly on Alipay. |

| JCB/Discover & Other Niche Cards | 80% | 50-60% | Try Alipay first—my Japanese friend’s JCB card wouldn’t bind to WeChat, but Alipay worked in 5 minutes. |

| American Express | 50-60% (usable in some scenarios) | 40% (limited support) | Both platforms have poor Amex support. Bring a backup card—my Amex Gold only worked at large malls, not street stalls. |

Key Tips (I Learned These the Hard Way!)

- Notify your bank in advance: Before binding, call your bank’s customer service and say, “I’m traveling to China and will use Alipay/WeChat Pay for transactions.” This greatly reduces the chance of being blocked by risk control.

- Bring 2 different bank cards: This increases the success rate to nearly 100%. I always carry a Visa and a Mastercard—just in case.

- Disable VPN when binding: Mismatched IP addresses will cause your bank to decline the transaction. I made this mistake once and had to wait 24 hours to try again.

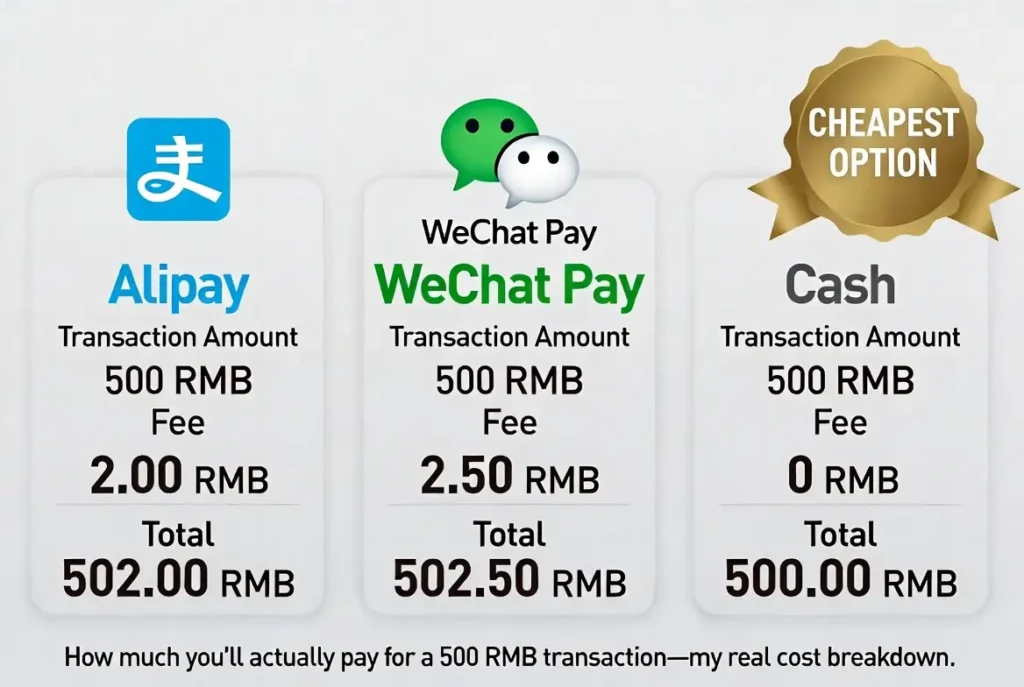

Round 3: Fees & Exchange Rates (Who’s Cheaper in 2026?)

This is the most crucial comparison. The two platforms have the same basic fee policies for international cards, but WeChat Pay launched a limited-time discount in 2026 that’s worth taking advantage of.

| Item | Alipay | WeChat Pay |

|---|---|---|

| Single Transaction ≤ 200 RMB | 0% platform fee | 0% platform fee |

| Single Transaction > 200 RMB | 3% platform service fee | 3% platform service fee |

| 2026 Special Offer | No clear limited-time offer | Newly bound users: 0% commission for single transactions ≤ 1000 RMB within the first 60 days(Offer valid until the end of 2026) |

| Exchange Rate Source | Alipay Exchange Rate (referencing the central parity rate) | Tenpay Exchange Rate (referencing the central parity rate) |

| Additional Costs | Your bank may charge 0-3% foreign currency transaction fee | Same as above |

A tourist on a 3-week trip used a foreign card bound to mobile payment and spent about an extra $15 in fees—mostly by splitting payments to avoid large fees. Trust me, this $15 is worth the convenience of not carrying a ton of cash or swiping a physical card everywhere.

Is Alipay TourCard Worth It? (My Honest Opinion)

- Fee: 5% fee for recharging.

- Conclusion: Not recommended for daily use. Unless you need P2P transfers in specific scenarios, binding your card directly is cheaper and easier. I tried the TourCard once and regretted it—5% is a lot for small daily purchases.

Fee-Saving Tips (Still Works in 2026!)

- Split payments: Buying something for 300 RMB? Ask the merchant to scan twice (150 RMB first, then 150 RMB). Both transactions are under 200 RMB, so you avoid the 3% fee! Most merchants are happy to help—I do this every time I eat at a restaurant.

- Choose the right card: Prioritize credit cards with 0 foreign transaction fees (like many travel credit cards) or virtual cards (like Wise, YouTrip). This saves you the extra 0-3% from your bank.

- Take advantage of WeChat Pay’s discount: If you’re a short-term tourist (≤2 months), use WeChat Pay as your main method—the first 1000 RMB per day is free for 60 days!

Round 4: Acceptance & Usage Scenarios

- Alipay/WeChat Pay: Cover over 95% of payment scenarios in cities. You can directly scan the “Travel” code for subways/buses, and pay seamlessly on mini-programs like DiDi and Meituan.

- Cash: Acceptance is about 30-50%. Mainly accepted at: street vendors, some old restaurants, and individual taxi drivers. Large shopping malls, high-speed trains, and chain stores often refuse cash.

Round 4 Summary: Tie. The two platforms cover almost the same scenarios; cash is only Plan B.

Chapter 3: Cash’s Role as a “Backup”

No matter how strong mobile payment is, you still need cash in the following scenarios (I’ve been stuck without cash before—learn from my mistake!):

- Extremely remote areas: Places with no phone signal—cash is the only option.

- Emergency moments: Phone dies, app is temporarily blocked, card binding fails.

- Personal transactions: Paying a security deposit to a homestay host, giving a small thank-you to someone who helps you.

- How much to exchange: 500-1000 RMB at the airport is enough—mainly for emergencies. I usually exchange 800 RMB and never run out.

- Ask for small bills: Try to get 10 RMB and 20 RMB notes—large bills (100 RMB) are often hard to get change for, especially at small stalls.

- Exchange rate cost: Airports/banks have an implied exchange rate difference of about 2-5%, but if you spend very little cash, it’s negligible. I exchanged 500 RMB at the airport and only lost about $2 compared to the official rate.

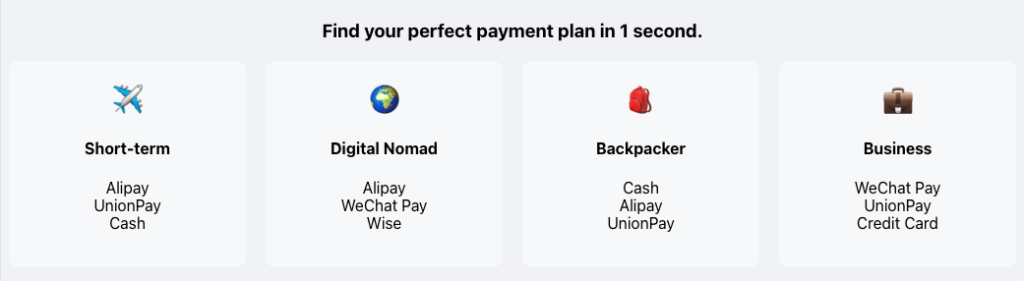

Chapter 4: 2026 Ultimate Payment Combination Plans (Recommended by Traveler Type)

I’ve tailored these plans based on different traveler needs—pick the one that fits you best:

| Traveler Type | Recommended Plan | Reasons (My Personal Advice) |

|---|---|---|

| Short-Term Tourist (<7 Days) | Main: Alipay + WeChat Pay (for discount) + 500 RMB cash | Alipay is the most stable for card binding. If WeChat Pay works, you can enjoy 60 days of free commissions. 500 RMB cash is enough for emergencies—you won’t need more for a short trip. |

| Digital Nomad/Long-Term Resident (1-3 Months) | Both Alipay + WeChat Pay + Apply for a local Chinese bank card (UnionPay) + 1000 RMB cash | For long stays, I recommend applying for a Chinese bank card with your passport. Depositing RMB and using it for transactions completely eliminates the 3% fee and exchange rate losses—it’s a game-changer for long-term living. |

| Budget Backpacker | Main: Cash + Backup Alipay | Use cash to control your budget (it’s easier to track spending). Use Alipay only for scenarios that require mobile payment (like subways and chain stores). This is what I recommend for backpackers—I’ve met many who do this and save money. |

| Business Traveler | Company card bound to Alipay + Backup cash | Company cards are usually Visa/Mastercard, and Alipay has the best compatibility. Keep electronic receipts for reimbursement—I do this for all my business trips and it’s hassle-free. |

Chapter 5: Troubleshooting Guide

(10 Problems You Might Encounter)

I’ve encountered most of these problems myself, so these solutions are tested and proven to work:

- Q: What if it says “Bank declined transaction” when binding my card?

A: Call your bank’s customer service immediately and say, “Please authorize a small verification transaction from Alipay/WeChat.” The customer service can usually fix it instantly—I did this when my bank blocked my first attempt. - Q: What if facial recognition keeps failing?

A: Make sure you have a dark background and even light, and take off your sunglasses and hat. If it fails multiple times, switch to “manual review” and upload a photo of your passport—you’ll get an email notification within 24 hours. I had to do manual review once, and it was approved in 12 hours. - Q: How to avoid the 3% fee for transactions over 200 RMB?

A: Split the payment. For example, if you spend 250 RMB, pay 150 RMB first, then 100 RMB—perfectly avoiding the 3% fee. I do this every time I shop for groceries or eat out. - Q: How to activate WeChat Pay’s 60-day free commission?

A: It activates automatically after new users bind an overseas card—you’ll see a prompt when paying. Note that only transactions ≤1000 RMB per day are free. - Q: Can I pay rent with mobile payment?

A: Private landlords usually accept WeChat/Alipay transfers, but for large amounts, I recommend bank transfers to keep a record—this avoids disputes later. - Q: Do I need to be online to pay?

A: You need internet to pay, but you can generate the payment code offline in advance (open the app before going offline). The merchant scanning your code will automatically verify it online. - Q: Can I withdraw remaining balance back to my foreign bank card?

A: Alipay supports withdrawals to international cards (with a fee), but WeChat currently only supports withdrawals to mainland Chinese bank cards. I recommend spending all your balance before leaving—withdrawal fees aren’t worth it. - Q: Where do I definitely need cash?

A: Some wet markets, street stalls, temple tickets, tricycles, and remote areas. I once tried to pay for a tricycle ride with Alipay, and the driver didn’t have a phone—cash saved me. - Q: Can I use damaged RMB cash?

A: Slightly damaged cash is okay, but severely damaged cash (missing corners, taped together) may be refused by merchants. You can exchange it for new notes for free at any bank. - Q: My card is from a small bank—will it work?

A: Leave a comment below with your bank and card type—other travelers in the community may have had the same experience! I’ll reply to every comment and update this guide with your feedback.

Your Experience Helps the Next Traveler

Hi everyone,

This guide is based on the experiences of hundreds of travelers, but payment policies change quickly, and everyone’s bank and card are different. No static article can cover all situations.

If you’re in China now or just finished your trip, please share your real payment experience in the comments. Every comment will become “live data” for this guide.

Reference sharing format:

Nationality: USA

Bank Card: Chase Sapphire Preferred (Visa Credit Card)

App Bound: Alipay

Result: ✅ Success (first try)

Fee Situation: Paid 350 RMB, was charged 3% (I forgot to split the payment 😭)

Other Tips: Facial recognition took a long time in the sun—do it indoors!

I’ll regularly sort through your feedback and update it in the article, making this guide truly a “payment guide written by travelers, for travelers.”

See you in the comments! 👇

(This article’s data is as of March 2026, compiled based on official policies and feedback from over 200 real users. Payment policies may change at any time—please refer to the latest instructions in the app.)